Most people think of a 401(k) or 457 plan as the go-to way to save for retirement. Your employer offers it, you put in some money, maybe they match it, and you hope it grows into a nice nest egg.

But here’s the truth: these plans were never designed to make you wealthy. They were created to benefit employers and shift retirement responsibility onto workers.

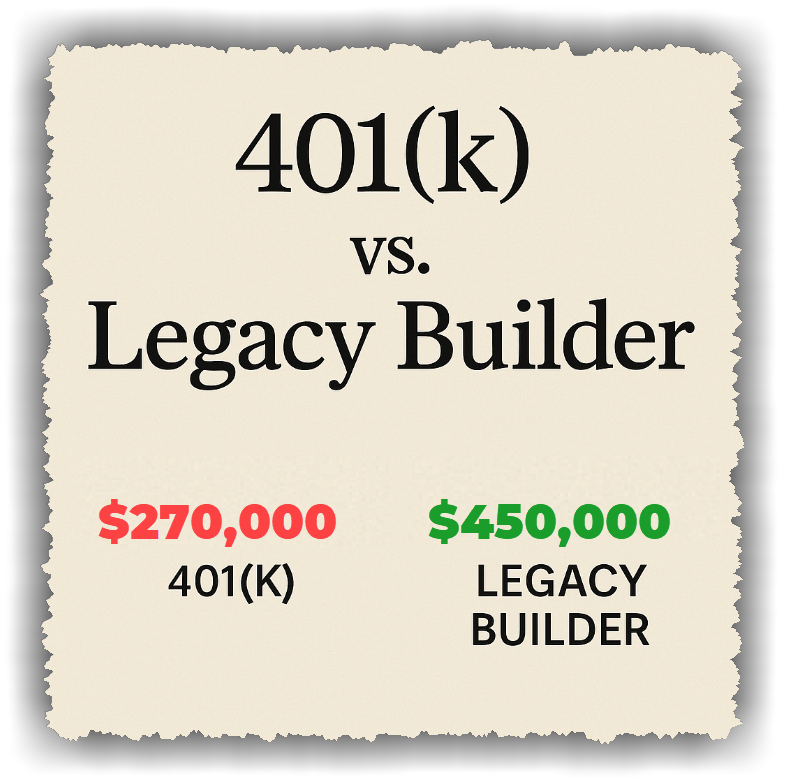

Let’s break down why 401(k)s and 457 plans exist, their tax benefits, the differences between the two—and why the Legacy Builder strategy can do far more for your wealth and your family’s future.

The Origin of the 401(k)

Before the late 1970s, retirement in America looked different. Most workers relied on pensions—defined benefit plans where employers promised a guaranteed monthly payment for life after retirement.

But companies didn’t like the long-term cost and liability of pensions.

-

In 1978, Congress passed the Revenue Act of 1978, which included Section 401(k) of the tax code.

DID I JUST SAY THE 401(k) WAS AN ACTUAL IRS TAX CODE?! 👀

And wait… 1978 was only 47 years ago. Oops, did I say that out loud?

-

In 1981, the IRS issued rules allowing employees to put pre-tax wages into 401(k) accounts.

-

Employers quickly shifted from pensions to 401(k)s, because it saved them money. Instead of guaranteeing lifetime benefits, they just offered a matching contribution and left the risk—and the responsibility—on the employee.

EMPLOYERS LEFT THE RESPONSIBILITY FOR RETIREMENT UP TO YOU.

So since they gave you a “choice,” why rely on the tool they created for their benefit to manage YOUR retirement?

Let. That. Sink. In.

So the 401(k) wasn’t invented to build massive wealth. It was a cost-saving move for companies.

Why People Use 401(k)s

401(k) plans have some perceived benefits:

✅ Pre-tax contributions lower your taxable income today.

✅ Tax-deferred growth means you don’t pay taxes until you withdraw.

✅ Employer matches can add “free” money to your account.

But here’s the reality:

❌ When you take money out in retirement, you pay ordinary income tax—and if tax rates rise in the future, you pay even more.

❌ If you withdraw before 59½, you’ll face a 10% penalty on top of taxes.

❌ At age 73, you’re forced to take required minimum distributions (RMDs) whether you need the money or not.

❌ You have no control over market swings or government tax changes.

In other words, you’re just delaying taxes—not eliminating them.

What About the 457 Plan?

A 457 plan is similar but is mostly for government workers and certain nonprofit employees.

✅ Penalty-free withdrawals when you separate from your employer (even if you’re younger than 59½).

✅ Still offers pre-tax contributions and tax-deferred growth.

✅ Often allows special catch-up contributions for people close to retirement.

❌ Not always protected under ERISA, meaning creditor protection can be weaker.

❌ Rollovers are more restrictive compared to 401(k)s.

Now, Let’s Look at the Legacy Builder Strategy

The Legacy Builder strategy isn’t about waiting until retirement to access your money. It’s about building an ecosystem of businesses and investments that produce cash flow today while creating generational wealth for tomorrow.

✅ Immediate Control of Your Money — deploy into income-producing assets right away.

✅ No Forced Withdrawals or Penalties — no government rules like RMDs.

✅ Strategic Tax Efficiency — C-Corps, Holding Companies, and Trusts minimize taxes legally.

✅ Cash Flow Over Simple Savings — your money works for you continuously.

✅ True Generational Wealth — leave companies and trusts, not tax-heavy accounts.

The Big Takeaway

A 401(k) or 457 locks up your money for 20–30 years. The Legacy Builder builds wealth and cash flow now, and leaves something real for the next generation.