DISCLAIMER: This article is for educational and informational purposes only and should not be interpreted as legal, tax, or financial advice. Business structures, taxation, and compliance requirements vary by situation, state, and federal law. Readers should conduct their own due diligence and consult qualified professionals regarding their specific circumstances.

Most entrepreneurs know how to make money.

Very few understand the system money operates inside of.

Most people were never taught:

- what tariffs are,

- why federal income taxes exist,

- why Social Security taxes come out of their checks,

- what Medicare actually is,

- why corporations became powerful,

- why LLCs were introduced,

- or how business structures evolved over time.

Instead, millions of entrepreneurs are told one simple sentence online:

“Just open an LLC.”

But business structure in America has a much deeper history than most people realize.

To understand why business owners today debate Sole Proprietorships, Partnerships, LLCs, S-Corps, and C-Corps, we first have to understand the financial history of the United States itself.

Because structure did not appear out of nowhere.

It evolved.

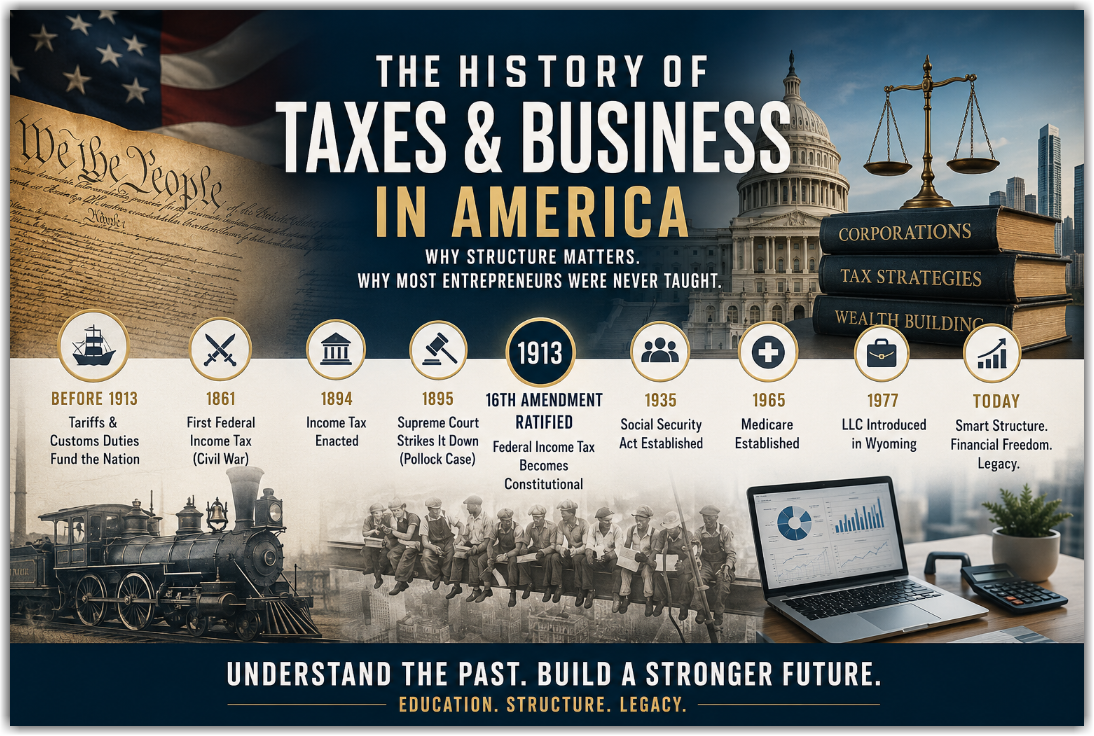

Before Federal Income Taxes: How America Originally Made Money

Before America had a permanent federal income tax, the federal government primarily funded itself through:

- tariffs,

- customs duties,

- and excise taxes.

What Is a Tariff?

A tariff is a tax placed on imported goods entering a country.

For example:

- imported steel,

- vehicles,

- clothing,

- tea,

- electronics,

- and manufactured products

can all be taxed when entering the United States.

For much of early American history, tariffs were one of the federal government’s primary revenue sources.

1789 — The Tariff Act of 1789

One of the first major laws passed after the U.S. Constitution was ratified was the Tariff Act of 1789.

The purpose was simple:

- generate revenue,

- protect American industries,

- and help stabilize the newly formed nation.

At the time, America did NOT operate with the permanent federal income tax system we know today.

In fact, for much of early American history, the average American did not pay federal income taxes on wages.

That alone surprises most people.

1861 — America Introduces Its First Federal Income Tax

The first federal income tax was introduced during the Civil War.

Why?

Because wars are expensive.

The government needed additional revenue to fund military operations.

This tax, however, was temporary.

After the Civil War, the income tax was eventually repealed.

But the idea of taxing income had now entered the conversation.

1894 — Congress Attempts Another Income Tax

As America industrialized and wealth expanded during the late 1800s, Congress attempted to establish another federal income tax through the Wilson-Gorman Tariff Act.

This created a constitutional debate that would change American history.

1895 — The Supreme Court Strikes It Down

In the famous:

Pollock v. Farmers’ Loan & Trust Co.

case, the Supreme Court ruled portions of the federal income tax unconstitutional because certain direct taxes were not apportioned among the states according to population.

That decision forced America back toward relying heavily on tariffs and excise taxes — at least temporarily.

But public pressure for a permanent income tax system continued growing.

1913 — The 16th Amendment Changes the Financial System Forever

Everything changed in 1913 with the ratification of the:

Sixteenth Amendment to the United States Constitution

This amendment gave Congress the constitutional authority to levy a federal income tax without apportioning it among the states.

This became the constitutional foundation for the modern federal income tax system.

But here’s something most entrepreneurs don’t realize:

The original federal income tax primarily targeted higher earners.

In the early years, many working-class Americans paid little or no federal income taxes at all.

Over time, however — especially during wars, economic expansion, and government growth — the tax system expanded dramatically.

Eventually, taxes became part of everyday American life.

Corporations Became Extremely Important

Long before LLCs existed, corporations were already major economic engines in America.

Corporations helped businesses:

- raise capital,

- separate ownership from operations,

- continue beyond the life of the founder,

- and scale far beyond what most sole proprietorships could accomplish.

Over time, corporations became central to:

- railroads,

- banking,

- manufacturing,

- industrial expansion,

- and eventually multinational commerce.

One of the most discussed corporate legal milestones is:

Santa Clara County v. Southern Pacific Railroad

which is commonly referenced in discussions surrounding corporate personhood and constitutional protections involving corporations.

Whether people agree or disagree with the broader interpretations of that case, one thing became clear:

Corporations became incredibly powerful in American business history.

Corporate Tax Rates Continued Rising

As America evolved, corporate tax rates increased dramatically during different periods in history.

At one point, corporate tax rates reached approximately 48%.

Now think about that for a moment.

If corporations were paying nearly half their income in taxes… wouldn’t business owners start looking for alternative tax treatment?

Of course they would.

And this is where modern pass-through taxation became increasingly attractive.

What Is Pass-Through Taxation?

Pass-through taxation generally means:

- the business itself does not pay federal income taxes at the entity level,

- and profits “pass through” directly onto the owner’s personal tax return.

This became attractive because many business owners wanted to avoid certain forms of double taxation associated with traditional corporate taxation.

Over time:

- sole proprietorships,

- partnerships,

- and eventually LLCs

became increasingly popular because of this flexibility.

But understanding WHY pass-through entities became popular historically matters.

Most people today simply hear:

“LLCs save taxes.”

without understanding the historical evolution behind that statement.

Sole Proprietorships: The Simplest Structure

A Sole Proprietorship is the default business structure for a single individual operating a business without formally creating a separate legal entity.

This means:

- the owner and business are generally treated as the same for tax purposes,

- profits and losses flow directly onto the owner’s personal tax return,

- and the owner may carry personal liability exposure.

Many businesses in America still begin this way today.

Partnerships: Shared Ownership

Partnerships allowed multiple individuals to operate businesses together while sharing profits and losses.

Like sole proprietorships, partnerships also became attractive because of pass-through taxation.

However, depending on structure and state law, partnerships could still expose partners to varying degrees of personal liability.

The LLC Didn’t Exist Until 1977

Read that again.

America was founded in 1776.

The LLC did not arrive until 1977.

That means corporations, partnerships, and sole proprietorships dominated American business for generations before LLCs ever existed.

This is one of the most misunderstood parts of modern entrepreneurship.

The first LLC law in the United States was introduced through the:

Wyoming Limited Liability Company Act

Wyoming created the LLC as a hybrid structure combining:

- limited liability concepts,

- with partnership-style pass-through taxation.

Why?

Because business owners were searching for more flexible tax treatment while still attempting to maintain liability protection.

Years later, the IRS provided additional clarity allowing LLCs to receive partnership-style tax treatment, which accelerated adoption nationwide.

By the 1990s, LLCs exploded in popularity across America.

However, something important is often overlooked.

The LLC was originally created to help solve a tax problem while limiting liability among multiple business partners. It was not originally designed around the idea of a single individual operating alone.

This is one reason the IRS often treats a single-member LLC as a “disregarded entity” for federal tax purposes by default — meaning the business activity generally flows directly onto the owner’s personal tax return similar to a sole proprietorship unless another tax election is made.

Understanding that historical context matters.

Because many entrepreneurs today are forming LLCs without understanding why the structure was originally created in the first place.

The Rise of the S-Corporation Election

Another major development was the S-Corporation election.

An S-Corp is NOT a separate entity created at the state level like an LLC or Corporation.

Instead, it is a federal tax election.

This election allowed certain businesses to receive pass-through taxation while operating under corporate structures.

Again, the pattern remained the same:

Business owners continued searching for legal ways to reduce tax burdens.

That has been happening throughout American history.

Social Security Taxes: Why They Exist

Many entrepreneurs pay taxes every year without fully understanding what those taxes actually fund.

What Is Social Security?

Social Security was established through the Social Security Act in 1935 during the Great Depression under President Franklin D. Roosevelt.

The purpose was to create a federal safety net for:

- retirees,

- disabled individuals,

- surviving family members,

- and dependents.

Social Security taxes are generally collected through payroll taxes under FICA (Federal Insurance Contributions Act).

The system was designed so workers contribute during their working years to support future benefits.

Medicare: Healthcare Support for Older Americans

What Is Medicare?

Medicare was established in 1965 to provide healthcare coverage primarily for older Americans.

Before Medicare, many seniors struggled to obtain affordable health insurance.

Like Social Security, Medicare became a major component of the American social safety net.

Payroll taxes became one of the primary funding mechanisms supporting these programs.

From Pensions to 401(k)s: The Shift in Financial Responsibility

Years ago, many Americans relied heavily on employer pensions.

Companies would often provide retirement income after decades of employment.

Over time, however, America gradually shifted toward self-funded retirement systems such as:

- 401(k)s,

- IRAs,

- and individual investment planning.

This changed everything.

Financial responsibility increasingly shifted onto individuals.

Today, many Americans are expected to:

- build retirement savings,

- understand taxes,

- manage investments,

- operate businesses,

- and create wealth

without ever being formally educated on how the financial system actually works.

That’s the real problem.

Not lack of ambition.

Lack of education.

Modern Entrepreneurship and the “Just Open an LLC” Era

Fast forward to today.

Millions of entrepreneurs are opening businesses through:

- TikTok videos,

- Instagram clips,

- YouTube Shorts,

- online influencers,

- and simplified internet advice.

Unfortunately, many people are starting businesses without understanding:

- taxation,

- bookkeeping,

- compliance,

- structure,

- separation,

- liability,

- or long-term planning.

Many entrepreneurs are operating businesses they believe are fully separate… while still remaining personally attached financially in multiple ways.

Structure matters.

Bookkeeping matters.

Compliance matters.

Understanding WHY these entities were created matters.

You cannot build a long-term legacy operating purely off social media soundbites.

Why Sophisticated Businesses Often Use Multiple Entities

As businesses grow, many entrepreneurs begin exploring:

- operating companies,

- parent companies,

- holding companies,

- trusts,

- and real estate structures such as REITs.

The goal is often:

- organization,

- scalability,

- operational separation,

- asset segregation,

- tax planning,

- and long-term legacy building.

This is one reason sophisticated businesses rarely rely solely on simplistic one-entity strategies.

Historically, large businesses evolved into layered structures for a reason.

Most Entrepreneurs Were Never Taught the System

This article is not about fear.

This is not about hype.

This is about education.

Most entrepreneurs were never taught:

- the history of taxation,

- why different entities exist,

- how retirement systems evolved,

- why payroll taxes exist,

- or how business structures changed throughout American history.

Instead, many business owners are trying to build wealth inside a system they were never taught to fully understand.

That knowledge gap is costing people years.

Why We Created the Legacy Builder Process

At MAC Enterprise Consulting, our mission has always been bigger than simply helping people file paperwork or “start a business.”

Our goal is to help entrepreneurs understand:

- structure,

- separation,

- compliance,

- bookkeeping,

- taxation,

- asset protection,

- and long-term strategic planning.

Because structure matters.

The truth is, most entrepreneurs are operating businesses without ever understanding:

- how taxes work,

- how wealthy businesses scale,

- how corporations protect assets,

- how holding companies operate,

- or how sophisticated businesses legally reduce taxable income through planning, reinvestment, and operational strategy.

That knowledge gap is costing people years.

This is exactly why we created the Legacy Builder process.

Ready to Build Your Legacy?

Most people spend their entire lives working for money without ever understanding the system money operates inside of.

The Legacy Builder was created to help entrepreneurs:

- structure properly,

- protect assets,

- build business credit,

- understand taxation,

- reduce liabilities,

- and position themselves for long-term financial freedom.

Stop building blindly.

Start building strategically.

References & Historical Sources

The historical and legal references used throughout this article are drawn from publicly available governmental, legal, and academic sources, including the United States Constitution, federal agencies, historical archives, and U.S. Supreme Court records.

Supreme Court of the United States. “Santa Clara County v. Southern Pacific Railroad Co., 118 U.S. 394 (1886).” Available at: Santa Clara County v. Southern Pacific Railroad

National Archives. “16th Amendment to the U.S. Constitution: Federal Income Tax (1913).” Available at: National Archives — 16th Amendment

Internal Revenue Service (IRS). “The Agency, Its Mission and Statutory Authority.” Available at: Internal Revenue Service (IRS)

Social Security Administration (SSA). “Historical Background and Development of Social Security.” Available at: Social Security Administration (SSA)

United States Senate Historical Office. “The Income Tax and the 16th Amendment.” Available at: U.S. Senate Historical Office

Tax Foundation. “Historical Corporate Income Tax Rates and Brackets.” Available at: Tax Foundation — Historical Corporate Tax Rates

Internal Revenue Service (IRS). “Federal Insurance Contributions Act (FICA).” Available at: IRS — FICA Overview

Centers for Medicare & Medicaid Services (CMS). “History of Medicare and Medicaid.” Available at: Centers for Medicare & Medicaid Services (CMS)

Wyoming Legislature Archives. “Wyoming Limited Liability Company Act of 1977.” Available at: Wyoming Limited Liability Company Act (1977)

Supreme Court of the United States. “Pollock v. Farmers’ Loan & Trust Co., 157 U.S. 429 (1895).” Available at: Pollock v. Farmers’ Loan & Trust Co.

Until Reading this Blog i had no idea that Americans did not pay income taxes until 1861 even thou it was temporary. Really thinking back that is not that long ago. It was only 3% over $800 is crazy, but at the time i bet it was a scandal. I wish this was taught to me in school when i was a young.

This was a very interesting read.