How America Was Built on Corporations… Not LLCs And Why the LLC Timeline Changes the Entire Conversation

There is a widely repeated claim in modern business, legal, and tax conversations:

“LLCs have decades of case law and are well-established legal entities.”

At first glance, that statement appears accurate—measured, even authoritative.

But when examined through the lens of legal history, statutory development, and federal recognition, it becomes clear that this claim is often presented without critical context.

Because the truth is not simply about whether LLCs have case law.

The truth is how much, where it comes from, and what it is built upon.

PART I: BEFORE THE LLC — THE ARCHITECTURE OF AMERICAN WEALTH

Long before the concept of a Limited Liability Company existed, the United States had already developed:

- National banking systems

- Industrial manufacturing empires

- Railroad infrastructure

- Oil monopolies

- Insurance institutions

- Universities and philanthropic foundations

These systems were not experimental.

They were not fragmented.

They were built using one primary legal vehicle:

👉 The corporation

The Legal Foundation: Corporate Personhood

The concept of a business entity operating as a “person” within the legal system is not modern.

It is rooted in centuries of legal doctrine and reinforced in U.S. law through:

- Santa Clara County v. Southern Pacific Railroad

This case is widely recognized for affirming that corporations are entitled to protections under the Equal Protection Clause of the 14th Amendment.

What This Means Structurally

A corporation can:

- Own property

- Enter contracts

- Sue and be sued

- Exist independently of its owners

This is not merely a state-level construct.

👉 It is interwoven into federal constitutional interpretation

Historical Reality

By the time the 20th century began:

- John D. Rockefeller had already built Standard Oil (1870)

- Cornelius Vanderbilt had dominated transportation

- Henry Ford had revolutionized manufacturing

All through corporations.

Not LLCs.

Because LLCs did not exist.

PART II: THE INTRODUCTION OF THE LLC — A MODERN LEGAL DEVELOPMENT

The Limited Liability Company is not a historical foundation of American business.

It is a late 20th-century statutory innovation.

The Starting Point

- Wyoming → 1977 (First LLC statute)

This is the origin.

Not an evolution.

Not a refinement.

👉 A starting point

Federal Recognition Came Later

- Internal Revenue Service → 1988 (Rev. Rul. 88-76)

- IRS “Check-the-Box” Regulations → 1997

Interpretation

For over a decade:

- LLCs existed in limited jurisdictions

- Federal tax treatment was unclear

- Adoption was minimal

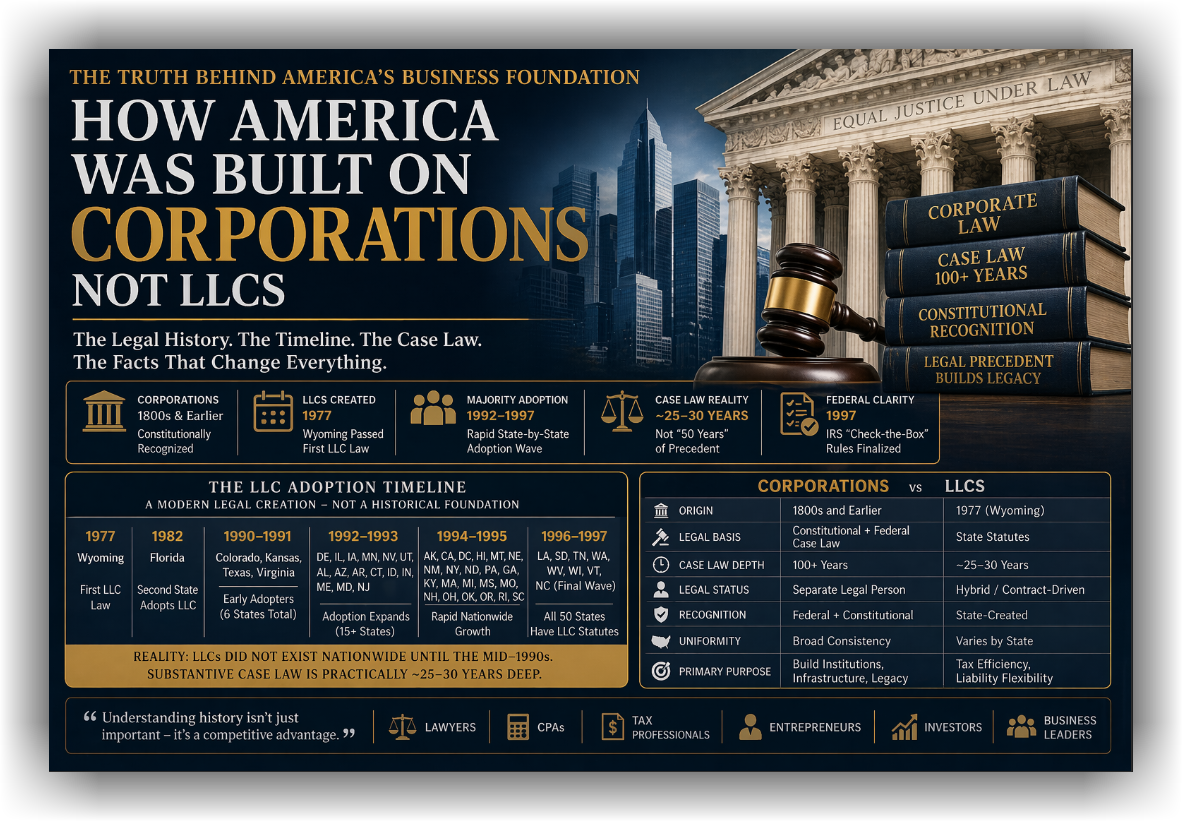

PART III: THE LLC ADOPTION TIMELINE — FULL NATIONAL CONTEXT

This is the part rarely shown in professional discussions.

Because once you see it, the narrative changes.

PHASE 1: LIMITED EXISTENCE (1977–1989)

| Year | States |

|---|---|

| 1977 | Wyoming |

| 1982 | Florida |

👉 For 12 years, only two states recognized LLCs.

PHASE 2: EARLY EXPANSION (1990–1991)

| Year | States |

|---|---|

| 1990 | Colorado, Kansas |

| 1991 | Texas, Virginia |

👉 Total states by 1991: 6

PHASE 3: RAPID ADOPTION (1992–1996)

1992

Delaware, Illinois, Iowa, Minnesota, Nevada, Utah

1993

Alabama, Arizona, Arkansas, Connecticut, Idaho, Indiana, Maine, Maryland, New Jersey

1994

Alaska, California, D.C., Hawaii, Montana, Nebraska, New Mexico, New York, North Dakota, Pennsylvania

1995

Georgia, Kentucky, Massachusetts, Michigan, Mississippi, Missouri, New Hampshire, Ohio, Oklahoma, Oregon, Rhode Island, South Carolina

1996

Louisiana, South Dakota, Tennessee, Washington, West Virginia, Wisconsin, Vermont

PHASE 4: NATIONAL COMPLETION (1997)

| Year | States |

|---|---|

| 1997 | North Carolina (final adoption phase) |

Simultaneously:

👉 IRS finalizes classification rules

CRITICAL ANALYSIS: WHAT THIS TIMELINE ACTUALLY MEANS

By applying basic legal reasoning:

1. Case Law Cannot Precede Existence

A structure must:

- Exist

- Be used

- Be litigated

- Be appealed

2. Realistic Legal Development Window

Although created in 1977:

- Minimal use until 1990s

- Widespread use begins mid-1990s

- Litigation develops late 1990s onward

👉 Substantive LLC case law is realistically ~25–30 years deep

3. Jurisdictional Limitation

LLC law is:

- State-specific

- Non-uniform

- Contract-driven (operating agreements)

4. No Constitutional Foundation

Unlike corporations, LLCs are:

- Not derived from constitutional interpretation

- Not tied to federal personhood doctrine

- Not reinforced through Supreme Court precedent in the same manner

PART IV: CORPORATIONS VS LLCs — A STRUCTURAL DISTINCTION

Corporations

- Origin: 1800s and earlier

- Legal Basis: Constitutional interpretation + federal case law

- Structure: Independent legal person

- Case Law Depth: 100+ years

LLCs

- Origin: 1977

- Legal Basis: State statutes

- Structure: Hybrid entity (often pass-through)

- Case Law Depth: ~25–30 years (practically speaking)

PART V: THE STANDARD OIL MOMENT — WHERE STRUCTURE EVOLVED

- Standard Oil Co. of New Jersey v. United States

This case did not just break up a monopoly.

It created a blueprint:

- Multiple corporations

- Centralized control

- Distributed operations

Resulting Structure

- Holding companies

- Parent companies

- Subsidiaries

This remains the dominant structure today.

PART VI: THE ECONOMIC SHIFT THAT INTRODUCED LLCs

In 1977:

- Corporate tax rates approached 48%

This created demand for:

- Pass-through taxation

- Simplified ownership structures

- Reduced corporate-level taxation

The LLC Solved a Tax Problem

Not a historical one.

Not a constitutional one.

👉 A tax efficiency problem

PART VII: REFRAMING THE “50 YEARS OF CASE LAW” ARGUMENT

When someone says:

“LLCs have 50 years of case law”

A more precise statement would be:

“LLCs began in 1977, were widely adopted in the 1990s, and have developed state-level case law over the past 25–30 years.”

That is factually accurate.

And significantly different.

FINAL ANALYSIS

America’s economic infrastructure—

- Banking

- Energy

- Manufacturing

- Transportation

- Institutions

—was built long before LLCs existed.

Corporations were:

- The original structure

- The tested structure

- The federally recognized structure

LLCs are:

- A modern statutory creation

- A flexible tax tool

- A state-level legal construct

FINAL STATEMENT

You cannot fully understand modern business structure without understanding that corporations built the system—and LLCs were introduced later to adapt to it.

FOR THE SERIOUS READER

This is not an argument against LLCs.

It is an argument for historical accuracy and structural awareness.

Because the difference between:

- State statute

- Federal recognition

- Constitutional grounding

…is not academic.

👉 It is foundational.

REFERENCES & SOURCES

Primary Legal & Historical Sources

- Santa Clara County v. Southern Pacific Railroad

Established recognition of corporate rights under the Equal Protection Clause of the Fourteenth Amendment. - Standard Oil Co. of New Jersey v. United States

Established modern antitrust doctrine and led to the development of multi-entity corporate structures.

LLC Formation & Legal Development

- Wyoming Limited Liability Company Act (1977) – First statutory authorization of LLCs in the United States

- Development of LLC statutes across the U.S. (1992–1997 adoption wave)

- Confirmation that 40+ jurisdictions adopted LLC statutes between 1992–1997

- Historical summary of LLC creation and delayed recognition

IRS & Federal Tax Classification

- Internal Revenue Service Revenue Ruling 88-76 (1988)

Established partnership tax treatment for Wyoming LLCs, triggering national adoption trends - IRS “Check-the-Box” Regulations (Treas. Reg. §301.7701, effective 1997)

Allowed entities to elect tax classification and significantly accelerated LLC usage - Historical analysis of entity classification and federal tax treatment evolution

Adoption Timeline & Structural Growth

- Confirmation that LLC adoption was minimal until federal clarity (1988–1997)

- Documentation that all 50 states adopted LLC statutes by 1996–1997

- Analysis showing LLC growth accelerated only after federal tax clarity

Legal Commentary & Academic Analysis

- Hamill, Susan Pace. The Story of LLCs: Combining the Best Features of a Flawed Business Tax Structure

University of Alabama School of Law - Bishop, Carter G. Status Liability and the Single-Member LLC Perspective

Suffolk University Law Review - Wolters Kluwer. Understanding LLC Law: Its Past and Its Present

Historical Context: Pre-LLC Business Structures

- Corporate dominance prior to 1977 as the primary limited liability structure

- Evolution of entity classification under IRS Kintner Regulations (pre-1997)

Corporate Tax Context

- Historical U.S. corporate tax structure and rate evolution (mid-20th century to modern era)